Summer 2026 newsletter: Help someone who’s suffering

Talking to someone facing challenges

Here’s an insightful quote from The Boston Globe:

…when you’re in conversation with someone dealing with formidable challenges, don’t rush in with solutions or advice. Instead, ask: Would you prefer to be hugged, helped, or just heard? It’s such a simple tool, but it isn’t always the first response that occurs when someone is suffering.

I think this is great advice you can apply to clients, family members, friends, and others facing any kind of challenge. As an introvert, I think I’ll have a hard time offering a hug, but I’ll try to loosen up. Meanwhile, I’d love if fewer people rushed to give me advice when I mention a problem.

This advice appeared in “How to talk to someone with cancer” by Annabelle Gurwitch. I’ve put her The End of My Life Is Killing Me: The Unexpected Joys of a Cancer Slacker on my reading list.

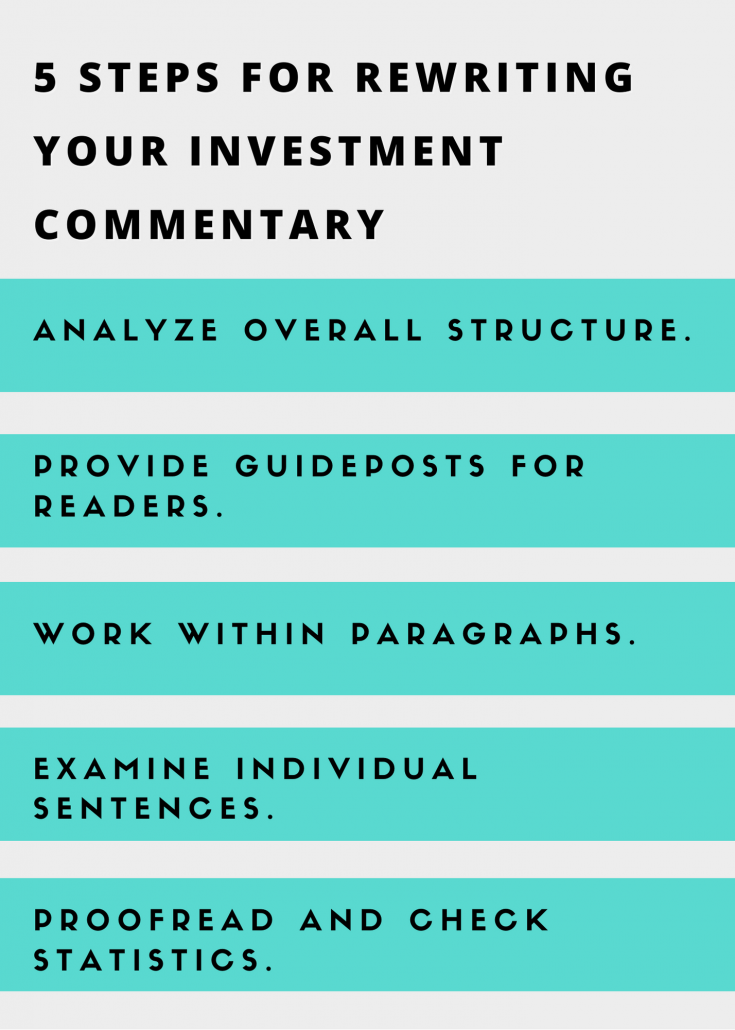

Need to edit your investment commentary?

Would you like to boost the impact of your quarterly commentary? Read my “5 steps for rewriting your investment commentary” for helpful tips.

In praise of the em dash

I am a big believer in em dashes, despite some clients shunning them to their association with writing generated using artificial intelligence (AI). If you are too, I think you’ll enjoy “Leave the em-dash alone.”

As author Colin Gorrie says, “Em-dashes aren’t the thing that makes AI writing bad.”

Rather:

AI prose has no sense of proportion. It deploys the same level of special effects to every sentence regardless of importance. It’s just always on. And this makes reading it exhausting: it’s just one zinger declarative sentence after another, without a pause to let you digest.

Has your vision worsened, or do your progressive lenses need to be reground?

An error in how my progressive lenses were ground made me stop reading printed books and I couldn’t read my computer screen without magnification or an oversized monitor. I asked my eye doctor why I couldn’t read magazines or books even though eye tests suggested that my vision was good. He said that the vision test numbers don’t tell the whole picture.

However, after years of believing that my vision had deteriorated in mysterious ways, I learned that my inability to read books and my computer monitor was in fact due to a problem with my glasses.

The good news: I don’t need my prescription computer glasses to read my monitor and I can read printed books and magazines again. The optometrist reground my lenses, and now I see much better.

The bad news: I never really needed my expensive prescription computer glasses. The dividing line in my progressive lenses was in the wrong place. As a result, I was trying to read computer monitors and print materials using the far vision part of my lens. I wish that my opthalmologist had suggested that I get my glasses tested for the correct placement of the dividing line.

Hackers use phony invitations to target you

An unexpected party invitation from a friend might actually come from a hacker. That’s what I discovered when I received what appeared to be a Paperless Post invitation from a friend. Something didn’t seem right, so I emailed the friend’s wife to ask if that was a legitimate invitation. No, it was not.

You can learn more about this phenomenon in “Spotting fake Paperless Post emails and spam texts: How to know what’s real” or “There’s a New Phishing Scam: Fake Invitations.”

Happy summer!

I love watching flowering trees emerge in the spring, and now I’m looking forward to the growth of flowers, vegetables, and herbs.

I spotted these cherry blossoms in Boston this spring.

What my clients say about me

“Fast, effective, insightful. I can think of no better resource for superior financial writing.”

“Fast, effective, insightful. I can think of no better resource for superior financial writing.”

“Susan has an exceptional ability to tailor investment communications to the sophistication level of any audience. She has an uncanny ability to make very complex investment and/or economic topics accessible and understandable to anyone.”

“Susan’s particularly good at working through highly technical material very quickly. That’s very important in this business. A lot of people are good writers, but they have an extensive learning curve for something they’re unfamiliar with. Susan was able to jump very quickly into technical material.”

Boost your blogging now!

Financial Blogging: How to Write Powerful Posts That Attract Clients is available for purchase as a paperback ($49, affiliate link).

Here’s what advisors say about my book.

- A great read for advisors who want to blog better—or learn how to start!

Michael Kitces, Nerd’s Eye View - Susan’s words have helped me hone my message and become clearer in my explanations. Through my dedication to blogging, my business has grown as a result. I owe much of my success in business to Susan’s teaching and guidance.

Dave Grant, Finance for Teachers - I wish I had read Susan’s Financial Blogging before I produced 300 weekly posts. There was a lot of practical advice in a slim 13- page guide to producing effective blogs. The blog preparation work sheets should be of particular value to an author who wishes to get smart people to do smart things with their money. My posts will be better for having read the book.

A. Michael Lipper, Mike Lipper’s blog